Item | Details |

Effective Date | April 2, 2026 |

Expiration Date | June 30, 2026 |

Validity Period | Approximately 3 months |

Policy Nature | Temporary, emergency tariff exemption |

Estimated Fiscal Cost | Approximately INR 180 billion |

Geopolitical conflicts in the Middle East (US-Israel-Iran conflict) have disrupted international crude oil shipping routes, leading to production cuts among Asian petrochemical enterprises. To ensure domestic supply stability and control manufacturing costs, the Indian government proactively reduced tariffs to boost imports and fill supply chain gaps.

The Indian Ministry of Finance has explicitly characterized this policy as a "temporary and targeted relief measure" in response to global supply chain disruptions caused by the West Asian conflict. It is not a long-term trade policy adjustment.

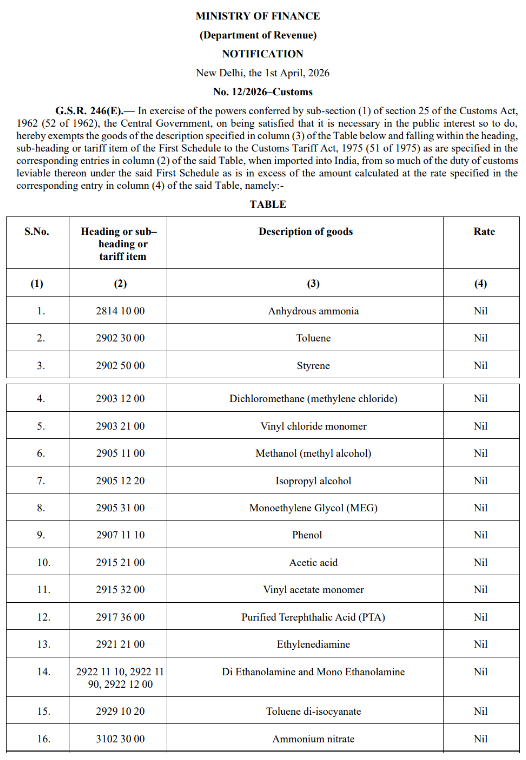

The zero-tariff policy covers over 40 chemical products across three major categories:

Category | Specific Products |

Basic Chemicals | Anhydrous ammonia, methanol, acetic acid, phenol, toluene, styrene, methylene chloride |

Intermediates | Vinyl chloride monomer (VCM), Purified Terephthalic Acid (PTA), Monoethylene glycol (MEG) |

Polymers/Resins | Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), PET resin, Polycarbonate (PC), ABS, SAN, Polyurethane (PU), Epoxy resin, Unsaturated polyester resin |

According to the Indian Ministry of Finance, the following industries will directly benefit:

Plastics & Packaging

Textiles

Pharmaceuticals

Chemical Manufacturing

Automotive Components

Other manufacturing sectors

Market Position in India: A major destination for Chinese PTA exports.

Trade Data:

Period | China's Exports to India | Share of China's Total PTA Exports |

Nov 2025 – Feb 2026 | 330,400 tons | 25% |

Jan-Feb 2026 | 128,000 tons | 21% |

Positive Factors:

Tariff Advantage: The previous ~3% tariff on Chinese PTA is eliminated, reducing import costs and enhancing competitiveness.

Delayed New Capacity in India: GAIL's new PTA capacity, originally scheduled for April 2026, has no confirmed commissioning date, sustaining import demand.

Cost Advantage: In March, the average PTA processing fee was only RMB 205/ton, unable to cover material costs. Large new domestic units have a significant cost advantage over older overseas plants.

Constraints:

Concentrated maintenance shutdowns for PTA plants in China in Q2 (involving 19.5 million tons of capacity) may limit export volumes due to lower domestic production.

Estimated PTA production in April is 6.03 million tons (down 670,000 tons from March).

Market Forecast: Monthly PTA exports are expected to rebound to between 400,000 and 430,000 tons

Market Structure in India:

Metric | Data |

Annual Demand | ~4 million tons |

Domestic Capacity | 1.59 million tons |

Import Dependence | >2 million tons (high external dependence) |

Main Applications | Pipes, profiles (driven by infrastructure and real estate) |

China-India Trade Status:

2025 China PVC exports to India: 1.5141 million tons, up 13.62% YoY.

Share of China's total PVC exports: 39.60% (i.e., nearly 4 out of every 10 tons exported go to India).

India is the largest core market for China's PVC exports.

Demand Match: India's PVC demand is primarily for general-purpose SG-5 resin, which aligns well with China's mainstream calcium carbide-based PVC. China holds a high market share in India due to geographical proximity, price advantages, and stable supply.

Policy Impact Analysis:

Level | Impact |

Indian Market | Quickly alleviates supply shortages, stabilizes prices, fills capacity gaps during the 3-month window. |

Chinese Exports | Offsets the cost pressure from the removal of the PVC export tax rebate effective April 1; exports expected to maintain high growth in Q2. |

Global Landscape | China's "cost advantage + policy dividend" dual benefit squeezes market share from SE Asian and Middle Eastern sources; accelerates the phase-out of high-cost overseas ethylene-based capacity. |

Cycle Logic: The industry shows a "policy clearance + supply contraction + geopolitical catalyst" triple resonance, further strengthening the PVC cycle reversal logic.

This is the most critical caveat of the policy.

The Indian Ministry of Finance's notification explicitly states: Existing anti-dumping and safeguard duties are unaffected and will continue to be levied on specific products and source countries.

According to analysis, 8 out of the 40 tariff lines are subject to anti-dumping duties. Exporters must:

Confirm their product's HS code is on the exemption list.

Verify if their product is subject to Indian anti-dumping or safeguard duties.

Recommendation: Ask Indian clients or a professional customs broker to verify; do not rely on experience alone.

Some analyses point out that while the basic customs duty is zero, considering other taxes (e.g., IGST 18%, social welfare surcharge), the total tax burden remains around 27.7%. The actual average reduction is only about 5 percentage points.

Regional supply tightness and ongoing logistics uncertainty may partially offset the benefits of the tariff concession. Actual import increases depend on the availability of supplies from exporting regions.

The policy is only a 3-month emergency measure. If the geopolitical conflict and raw material shortage are not resolved, the return to higher import costs after the policy expires could trigger renewed supply tightness.

Some local Indian analysts believe that if the Iran conflict persists, the government may extend the deadline and potentially reduce tariffs further. The policy's direction depends on:

Evolution of the Middle East geopolitical situation.

Recovery of international crude oil and raw material supplies.

Easing of India's domestic supply-demand imbalance.

Short-term: Benefits Chinese exports of PTA, PVC, and other products to India, aids destocking in Q2.

Medium-term: Accelerates the phase-out of high-cost overseas capacity, reshapes global trade flows.

Long-term: If geopolitical conflicts persist, India might normalize tariff relief, leading to sustained benefits for Chinese exports.

Check that your browser version is too low,

In order not to affect the normal use of the site, please directly upgrade your browser, or use other browsers such as: firefox, Google.